Indian travellers are able to make UPI payments, outside India. For this, all you need to do is enable international payment on your UPI app and scan QR codes to pay. However, it is not a cakewalk, like domestic UPI payments. Since international UPI payment is a still-developing project, UPI services are only available in selected countries and are enabled only by a few banks.

Here’s a quick video overview of using UPI outside India. Keep reading to learn how UPI works globally, how to set it up for each payment app, and its benefits and drawbacks.

List of UPI Accepted Countries 2024

Not all countries support UPI payments yet, so it’s important to know the regions where UPI is operational. The foreign countries that accept UPI payments, as of the year 2024, are as follows1:

- Bhutan

- France (ticket booking for Eiffel Tower)

- Mauritius

- Nepal

- Singapore

- Sri Lanka

- UAE

- Oman

- Japan

List of Banks that Support UPI International Payments 2024

To use UPI while travelling overseas, your bank must support UPI international transfers. So ensure that your UPI app is linked to the eligible bank account.

Banks that Support PhonePay International Payments

- HDFC Bank

- Axis Bank

- ICICI Bank

- State Bank of India

- Kotak Mahindra Bank

- Punjab National Bank

- Bank of Baroda

- Union Bank of India

- Canara Bank

- Indian Bank

- Central Bank of India

- IndusInd Bank

- UCO Bank

- Karnataka Bank

- DBS Bank

- AU Small Finance Bank

- Indian Overseas Bank

- Saraswat Bank

- South Indian Bank

- Punjab and Sind Bank

- City Union Bank

- Equitas Small Finance Bank2

Banks that Support PayTM International Payments

- HDFC Bank

- Indian Bank

- Axis Bank

- Central Bank of India

- ICICI Bank

- Bank of Maharashtra

- State Bank of India

- The Federal Bank Limited

- Kotak Mahindra Bank

- IndusInd Bank Limited

- Punjab National Bank

- Karur Vysya Bank Limited

- Bank of Baroda

- South Indian Bank Limited

- Union Bank of India

- City Union Bank Limited

- Canara Bank

- Punjab and Sind Bank

- Bank of India ESAF

- Small Finance Bank Limited3

Pro Tip: Remember to inform your bank about the dates of your international travel. If not, the bank might suspect your international payments as fraudulent transactions and freeze your account for security reasons.

How to Activate International UPI?

The process to enable UPI international payments is easy but differs for each payment app. Here’s a detailed pictorial guide, outlining the steps for the leading UPI payment apps in India.

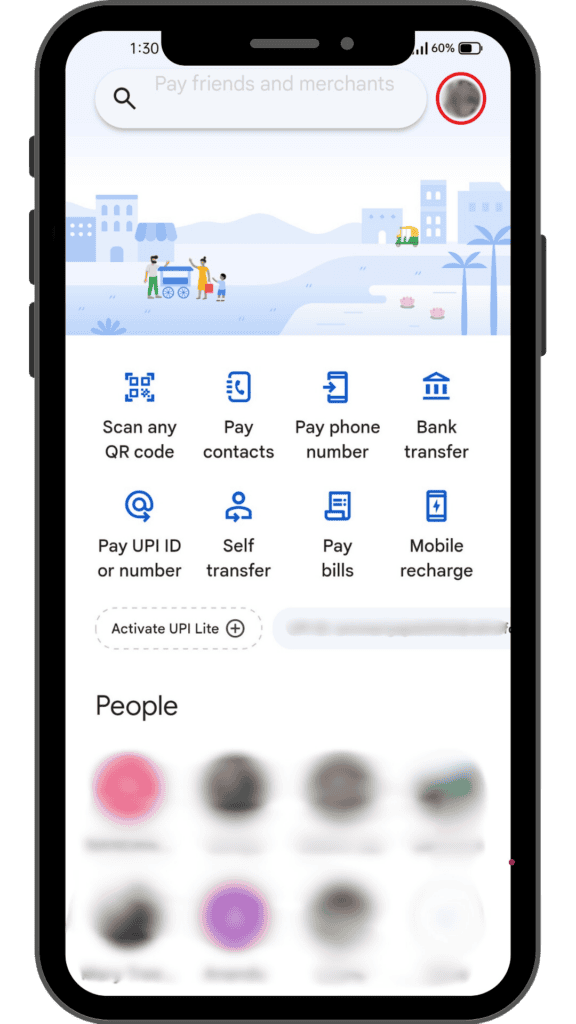

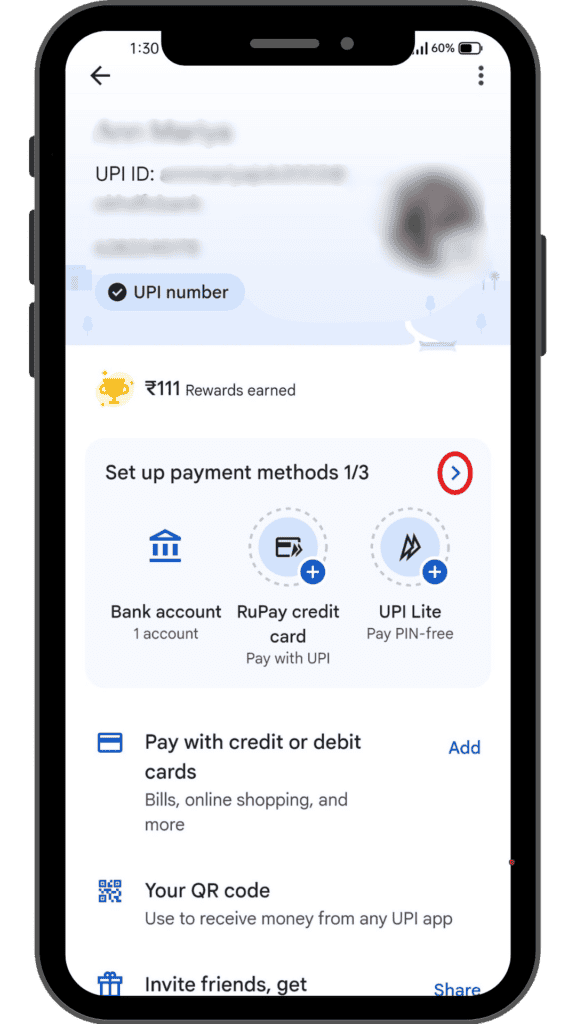

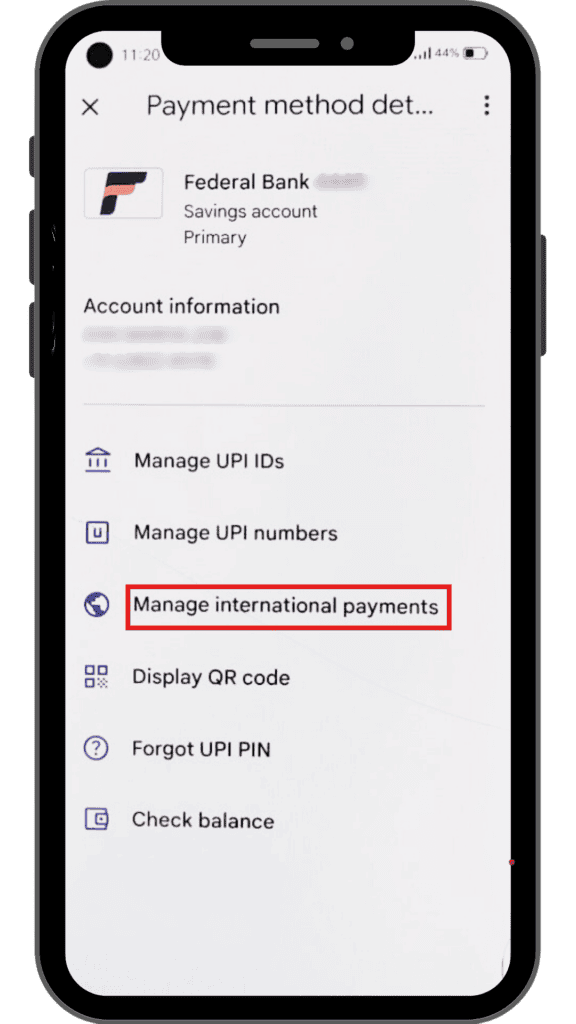

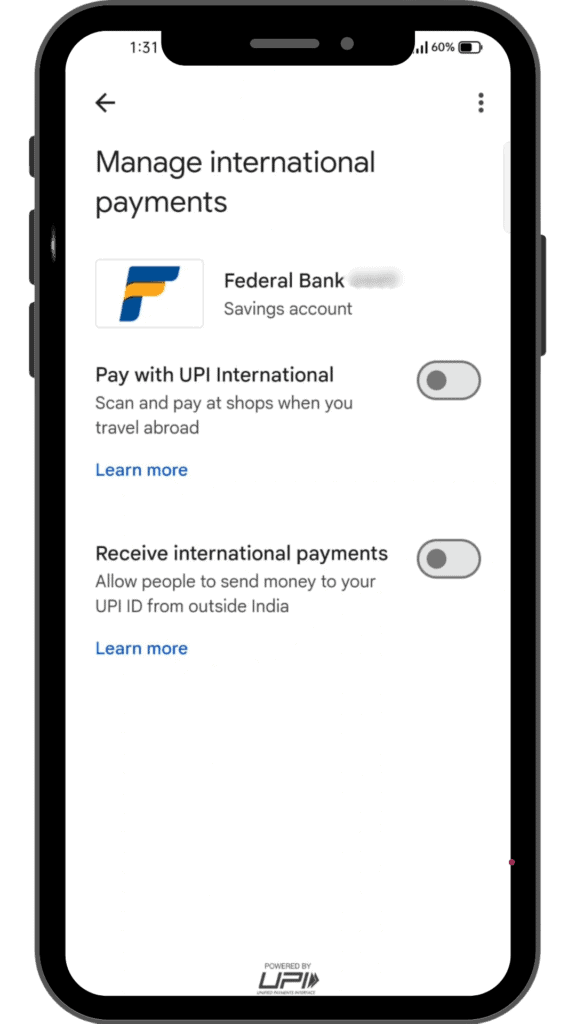

Steps to Activate International UPI on GPay4

1.Click on your profile picture on the GPay home screen.

2. Tap the arrow near the ‘Set up payment methods 1/3’ section.

3. Choose the bank account to be activated and under the ‘Payment method details’ page, select the ‘Manage international payments’ option.

4. Enable ‘Pay with UPI International’ and enter your UPI PIN.

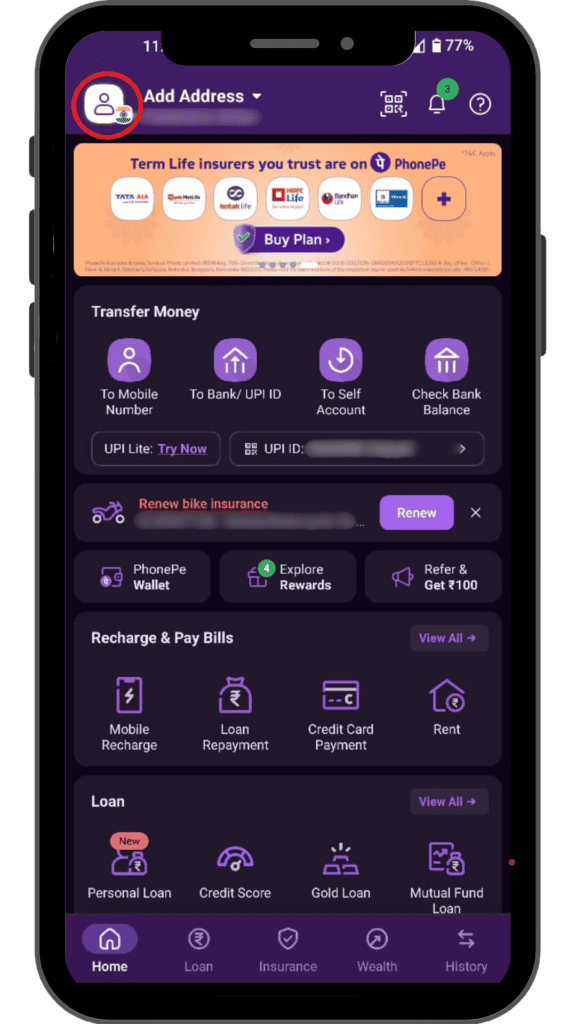

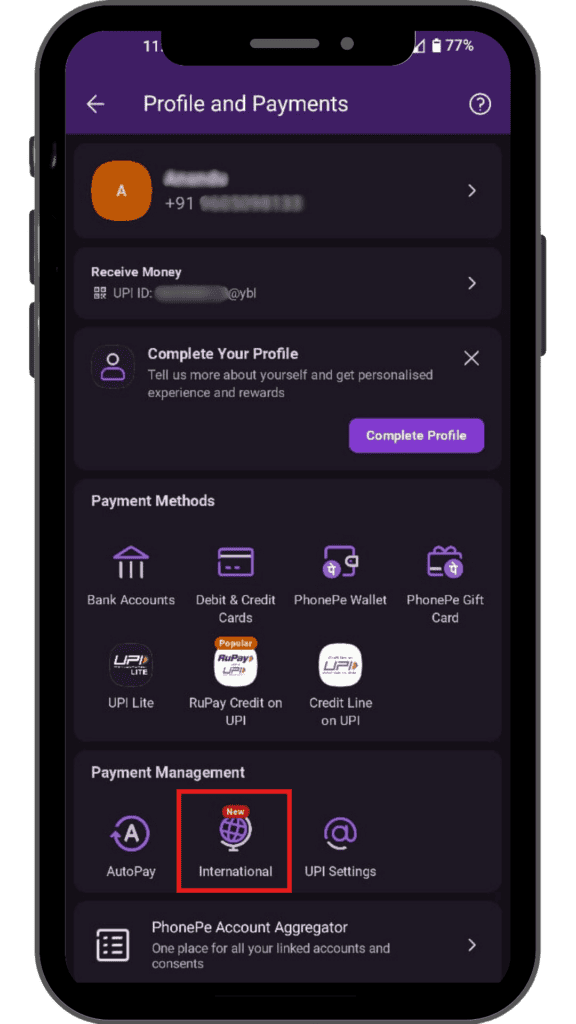

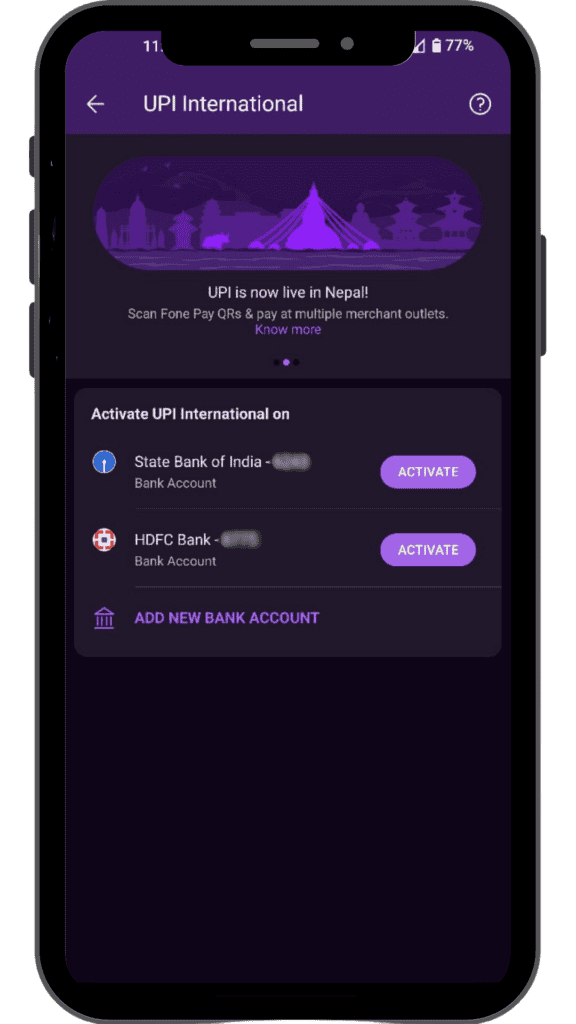

Steps to Activate International UPI on PhonePe5

1.Log in to your PhonePe app and click on your profile picture.

2. Within the ‘Payment Management’ section, select the ‘International’ feature.

3. Tap the ‘activate’ button for your preferred bank and enter the UPI PIN.

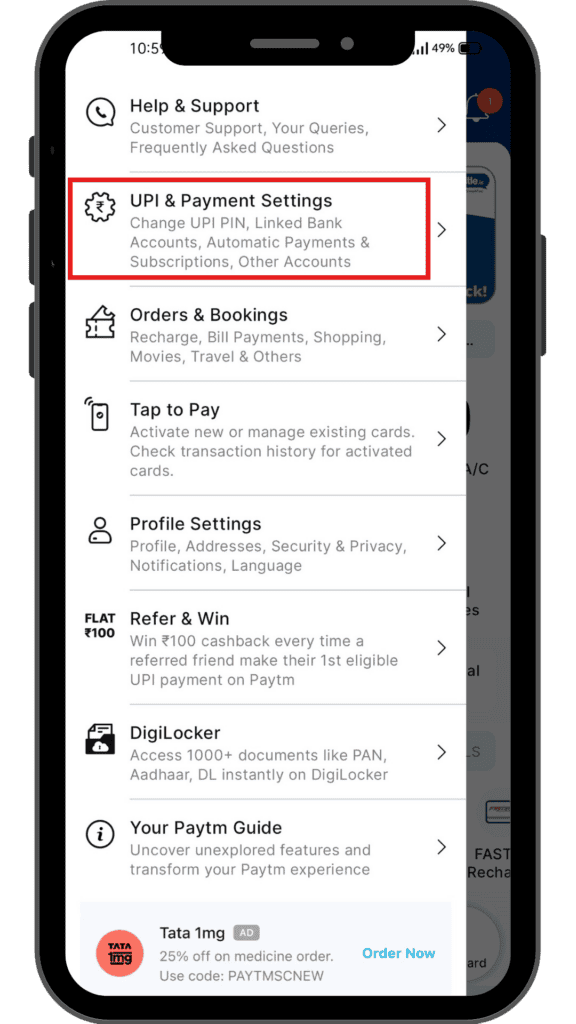

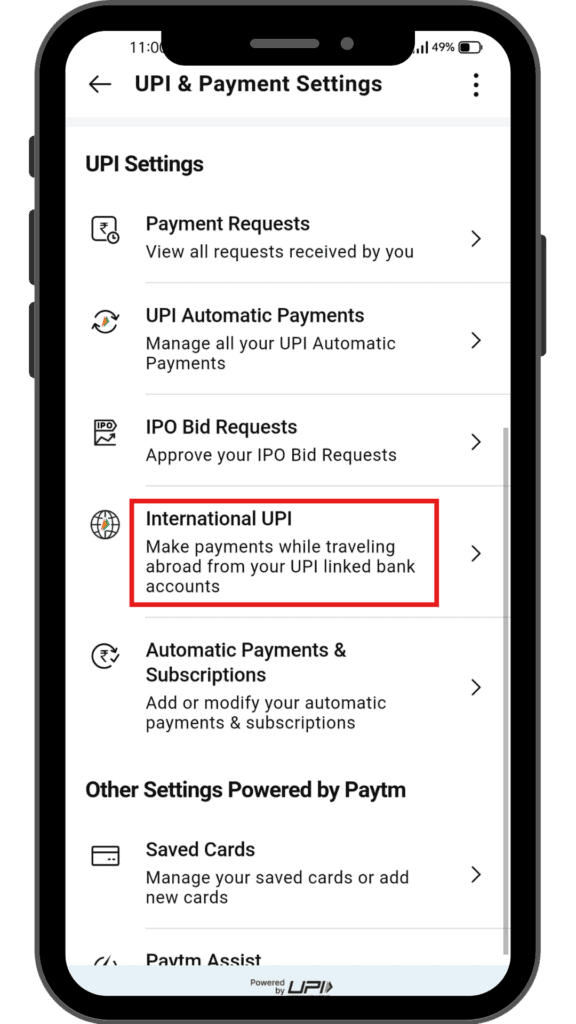

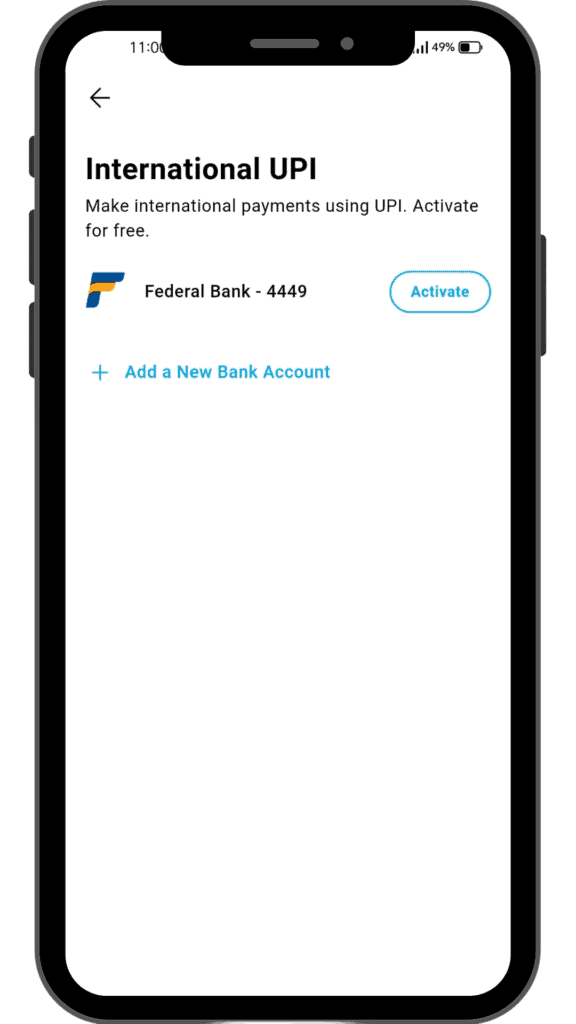

Steps to Activate International UPI on Paytm6

1.On the Paytm home screen, simply tap your profile picture to access your profile.

2. Scroll down and go to ‘UPI and Payment Settings’.

3. Below the ‘UPI settings’ section, select ‘International UPI’.

4. Enable the ‘Activate’ mode for your banking partner and enter your UPI PIN.

How to Do International Payments Outside India Using UPI?

Once you have activated international payment, you can pay easily using your UPI payment app.

1.Scan the QR code to pay.

2. Enter the amount in the foreign currency and the correspondent amount in Indian Rupees shall be displayed.

3. Choose the bank account.

4. The payment will be deducted from your bank account in INR, along with any applicable fees.

5. Verify by entering UPI PIN.

6. The amount shall be credited to the beneficiary bank account in the selected foreign currency.

UPI International Charges

Although international UPI transactions resemble domestic payments, the service is not free; it comes with several charges. However, these are not fees charged by the UPI payment app, but by your bank. This is because when you make a UPI payment abroad, it acts as an international bank transfer.7

These are the charges to anticipate while making international UPI payments:

- International transfer fees: These are charges imposed by banks to cover the cost of processing and handling the transfer across borders. They can vary depending on the bank, the amount being sent, and the destination country.

- Exchange rate markups: Instead of using the mid-market rate, banks and NPCI (UPI payment regulator) apply a higher rate to make a profit on the currency exchange.

- Conversion charge: Banks convert the Indian Rupees in your bank account into the desired foreign currency in real time. So for this service, they often charge a conversion rate.

| Types of Charges | Percentage Charged |

| International transfer fees | 2.5% |

| Exchange rate markups | 2% |

| Conversion charge | 3-5% |

International UPI Payment Limit

Foreign currency equivalent to below Rs. 2,00,000 is the per transaction limit for international UPI payments. This can differ according to your UPI app and bank terms and conditions.8

Limitations of Paying Abroad Using UPI

1. Limited Country and Merchant Support

UPI international payments are currently only available in limited countries. Within these countries, only specific merchants accept UPI, so its availability is reduced to certain areas or businesses.

2. Bank and App Compatibility

Not all Indian banks facilitate UPI international payments. So travellers must confirm that their bank and UPI apps are suitable to use abroad.

3. Currency Exchange Rate Fluctuations

UPI transactions abroad involve a currency conversion. Since the rate keeps on changing, it may rarely offer favourable rates.

4. Activation Validity

Once activated, you can pay internationally for only 7 days for GPay and up to 3 months for PayTM and PhonePe. However, you can reactivate the international mode as needed.

4. Security Concerns on Unsecured Networks

Using UPI abroad requires internet access, which may not always be secure. If travellers make transactions over public or unsecured Wi-Fi networks, they could be vulnerable to hacking and data breaches.

5. Dependency on Mobile Connectivity

UPI transactions rely on a stable internet connection, which may not always be available when travelling abroad.

What is the Better Option than UPI International?

While UPI International can be convenient, it’s not always the most cost-effective choice. Alternatives like purchasing foreign currency or using a single-currency forex card offer better control over costs and flexibility. Let’s explore these options:

1. Foreign Currency

Carrying foreign currency when travelling abroad is a straightforward solution. By purchasing currency from a trusted source like ExTravelMoney, you can lock in competitive rates and avoid the uncertainty of fluctuating exchange rates while abroad. This method is particularly useful for small transactions, tipping, or at places where card payments are not accepted.

2. Single-Currency Forex Card

A single-currency forex card allows you to load the foreign currency of your choice, lock the exchange rate, and spend abroad without worrying about conversion fees. Forex card is ideal for those who want a cashless way to manage their expenses abroad, all while keeping track of expenditures. Single currency forex cards only charge an ATM withdrawal fee of USD 2-3 per transaction and no other fees.

ExTravelMoney offers both these solutions, ensuring you get the best exchange rates. Whether you prefer carrying cash or using a Forex card, we make the process simple and affordable for you!

Also Read: How To Buy Forex Online In India

- NPCI Official Website ↩︎

- PhonePay International Payments ↩︎

- Paytm International Payments ↩︎

- GPay International UPI Activation ↩︎

- PhonePe International UPI Activation ↩︎

- PayTM International UPI Activation ↩︎

- GPay Bank and NPCI Charges ↩︎

- Paytm International Transaction Limit ↩︎

Ann Mariya Job is the Associate Content Writer at ExTravelMoney.com. Holding a Bachelor’s in Journalism, she excels in creating deeply researched, engaging, and crisp content. Her work helps readers understand the complexities of foreign exchange, overseas money transfers, and international travel.